“I have gone through around 40-50 pages till now. One thing I really liked is how easy it is to understand topics. For IBS (especially only Group 2 students ) that's probably more important than anything else. Happy with the purchase.

CA Final Student (Nov 26)

“There are honestly very few proper books available for IBS. I ordered this after seeing people recommend it in Telegram groups. Looks well thought out.

CA Final Student (Nov 26)

“Received the book today. First impression is really good. Quality feels premium and everything is arranged properly.

CA Final Student (Nov 26)

“I only have Group 2 left. My biggest concern was how to locate things quickly, especially for GR 1 topics during the paper. This book looks like it will make that much easier.

CA Final Student (Nov 26)

“I think this is one of those books where you can actually see the effort put into arranging the content.

CA Final Student (Nov 26)

“I was little hesitant because of the price initially. But after receiving the book I kind of understood why. The amount of effort and the way everything is organised makes sense.

CA Final Student (Nov 26)

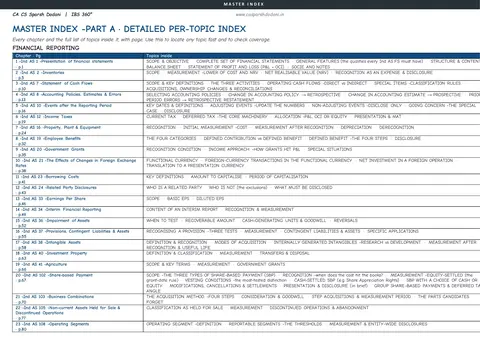

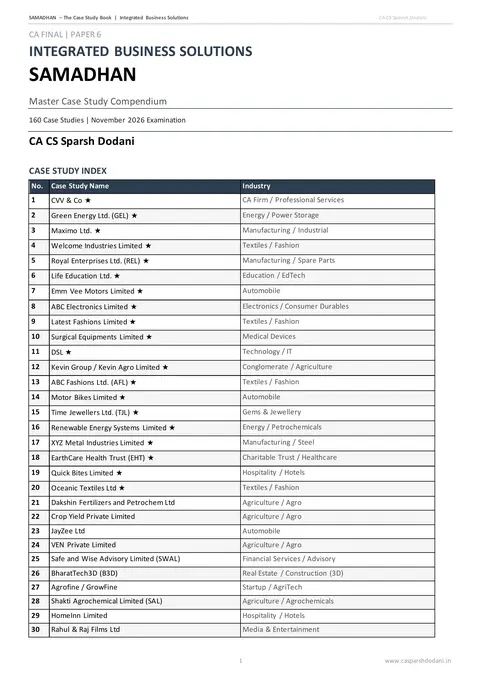

“I noticed few page number issues in the index, but before I could even message sir, there was already an update saying a complete master index would be shared.

CA Final Student (Nov 26)

“I dont usually give reviews this early but this one deserved it. IBS doesn't have too many quality resources and this one feels like it was actually designed keeping the exam in mind.

CA Final Student (Nov 26)

“Book is really good overall. Would have loved if font size was one point bigger because that would make navigation even faster. Apart from that, no complaints.

CA Final Student (Nov 26)

“Bought it because so many people were talking about it in CA groups. After spending some time with the book, I can understand why. It doesn't just have content, it makes finding the content easy.

CA Final Student (Nov 26)

“Book is slightly heavy 😅 but I guess that's because almost everything is covered in one place. Better than carrying 6-7 different books during the exam.

CA Final Student (Nov 26)

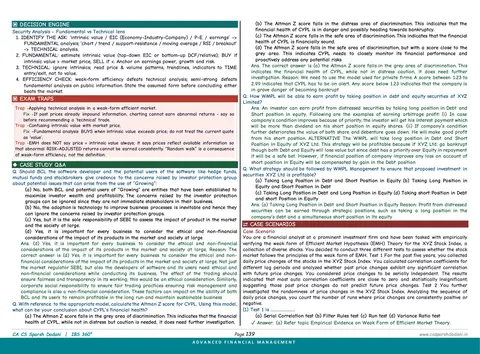

“Waiting for the decision engine and master index. If it is compatible the book, I think searching for different situations in the paper will become much easier.

CA Final Student (Nov 26)